Affirm: Buy now, pay over time

Affirm is the rare BNPL app that actually earns the 'transparent' label — it shows you the total dollar cost before you tap confirm, and its no-late-fees promise is real. But the headline '0% APR' is a best case, not a rule; on longer terms you can pay up to 36% APR, and the frictionless checkout can make it easy to spend more than you planned.

- Shoppers financing a specific big-ticket item (fridge, laptop, travel) who want fixed payments and a total cost shown upfront

- People who hate credit-card revolving debt and compound interest and want a defined payoff date

- Thin-file or credit-building users drawn to Affirm's soft pre-qualify and the 'real-time' underwriting it advertises for slim credit histories

- Anyone prone to impulse spending — the one-tap checkout removes the friction that normally slows you down

- People chasing rewards or cashback; a good rewards credit card paid in full beats this

- Shoppers who only buy small everyday items or shop mostly at stores Affirm doesn't support

- Anyone who assumes '0% APR' is guaranteed — many offers carry real interest

Overview

Affirm earns its 4.8 stars, and it earns them honestly — which is more than most of the buy-now-pay-later world can say. This is the BNPL app that tells you, in plain dollars, exactly what a purchase will cost you in total before you commit, charges nothing for a late payment, and never compounds interest against you. That’s a genuinely different posture from a credit card. But the app’s biggest marketing hook and its biggest honest caveat are the same fact: the interest. “0% APR” is real for some purchases at some retailers. For a lot of others, you’re looking at a rate that can climb to 36%. Read the number on the screen, every time, because it changes.

What Affirm actually is

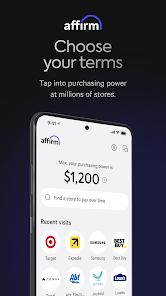

Affirm is a point-of-sale lender. You use it to finance a specific purchase — a $1,200 refrigerator, a $900 laptop, a flight — and instead of putting it on a revolving credit line, you agree to a fixed set of payments with a defined end date. That structural difference is the whole pitch. A credit card lets you carry a balance indefinitely and compounds interest on it; Affirm gives you a closed-end loan with a payoff schedule you can see from day one.

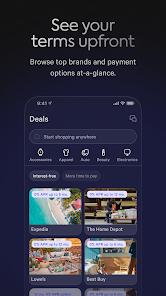

In 2026 the app is clearly trying to grow into something bigger than checkout financing. Affirm’s store copy pitches it as a “full-service banking alternative,” and the marketing promises a matching feature set: an Affirm Card (advertised as a virtual and physical card usable even at stores that don’t natively offer Affirm), a high-yield savings account, a “BNPL for Rent” pilot that splits rent into two payments, loan terms Affirm says stretch up to 48 months for large purchases, “real-time transaction analysis” underwriting pitched at thin-file users, and a price tracker for items in your cart. We’re repeating these as Affirm’s own claims about where the product is heading — not features we verified — and the newest, the rent pilot especially, read as roadmap rather than settled, universally available capabilities.

The 0% vs 0–36% reality

This is the part to internalize before anything else. Affirm’s marketing leans hard on “0% APR” and “zero compound interest,” and both can be true. But the app’s own FAQ states that rates run anywhere from 0% to 36% depending on your credit and the retailer. That’s an enormous spread. A 0% offer on a $1,000 purchase costs you exactly $1,000. The same purchase at 24% APR over a couple of years costs meaningfully more, and the longer the term, the more that gap widens.

Affirm’s saving grace is that it doesn’t hide this. Unlike a credit card, where the true cost of carrying a balance is buried in statements and compounding, Affirm shows you the total dollar amount you’ll repay before you confirm. One recurring review theme is exactly this: “they tell me the total dollar amount I’ll pay, no math.” That transparency is the product working as advertised. But transparency about a cost is not the same as the cost being low. A 36% loan is a 36% loan even when it’s honestly labeled. The right move is to check the number on every offer and, when it isn’t 0%, ask whether you’d still buy the item at that total.

Walking through the app

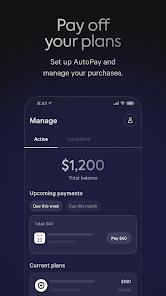

Pre-qualification is a soft credit pull, so checking what you’re eligible for doesn’t ding your score. That’s the low-risk on-ramp. The catch, spelled out in the FAQ: actually taking a loan may affect your score, and late payments feed Affirm’s own internal scoring even though they don’t generate a fee. So “no impact to check” and “no impact to borrow” are two different things.

At checkout, Affirm slots in as a payment option at supported retailers. You pick a term, see the fixed payment and the total, and confirm. The friction is low — which is the appeal and the risk in equal measure.

The Affirm Card is the workaround for Affirm’s biggest structural limitation: not every store supports it. You request a virtual card, add it to your mobile wallet, and use it more broadly. One reviewer described splitting a grocery-store payment this way. Useful, but worth noticing that it quietly extends BNPL from planned big purchases into everyday spending, which is precisely where the overspending risk lives.

The high-yield savings account is the banking-alternative play. Several users say it beats their local bank’s rate, and there’s no obvious reason to doubt that — high-yield accounts from fintechs generally do. Just don’t let the savings feature launder the impression that the whole app is a savings product. Its core business is lending.

What real users report

Across the 5-star reviews, the themes are consistent and believable. People finance a large necessity — a fridge, appliances — without draining their account at once, and feel relieved rather than trapped. The transparency lands: users repeatedly praise seeing the total upfront. The no-late-fee promise gets specifically validated (“was two days late from a bank error, not charged a cent”), which is a meaningful differentiator against credit cards that would have hit that person with a fee and a rate bump. And the Affirm Card plus savings features get called out as reasons people use it beyond one-off checkouts.

What’s notable is what these positive reviews don’t dwell on: the interest paid over the life of longer loans. That’s not a knock on the reviewers — it’s the nature of BNPL. The pain of interest is diffuse and future-tense; the relief of not paying $1,000 today is immediate.

Where it frustrates

The honest frictions are real and worth stating plainly. Interest on longer terms can make a purchase cost substantially more, and the “0% APR” framing sets an expectation many offers won’t meet. Overspending and debt-stacking is BNPL’s documented behavioral risk: frictionless installments make it easy to say yes, and easy to end up juggling several loans at once — a well-known pattern across the whole category, not unique to Affirm, but not solved by it either. Merchant coverage is incomplete; not every store supports Affirm natively, which is why the card exists. Purchases are usually skewed toward larger tickets, so it’s a poor fit if you mostly buy small items. And practically, it requires a US phone number, so it’s US-centric.

None of these are dark patterns — Affirm is unusually clean on that front — but they’re the reasons this isn’t a universal recommendation.

How it compares

Against Klarna and Afterpay, Affirm plays a different game. Those lean on short “Pay in 4” splits for smaller carts; Affirm’s strength is longer, larger financing with fixed terms and a total shown upfront, plus the card and savings layer. If you’re splitting a $60 order into four, Klarna or Afterpay are more natural. If you’re financing a $1,500 purchase over many months, Affirm’s transparency and no-compound-interest structure are the stronger proposition.

Against a credit card, the trade is clarity and no late fees versus flexibility and rewards. A rewards card paid in full every month beats Affirm outright — you get cashback and pay no interest. But for someone who would otherwise revolve a balance, Affirm’s fixed payoff and lack of compounding are genuinely safer. The comparison hinges entirely on your own discipline.

A note on recency

The app was last updated April 10, 2026, and the store listing advertises active 2026 development — the Affirm Card, the rent pilot, “real-time” underwriting, savings. On the strength of the changelog and rating this reads like a maintained, evolving product, not a coasting one. The flip side: the newest of those pitches (rent splitting especially) are early or roadmap, so treat availability and terms as things to confirm in-app rather than assume from the store copy.

The verdict

Affirm is the most honest player in a category that often isn’t, and for the right purchase — a real, planned, larger buy — its transparency, fixed payments, and zero late fees make it a defensible choice. Just don’t let “0% APR” do more work in your head than it does in reality. Check the total dollar cost on every offer, be honest with yourself about whether the frictionless checkout is helping you or nudging you, and remember that even the most transparent BNPL is still debt. Used deliberately, it’s a strong tool. Used impulsively, it carries the same risks, just more transparently presented.

How We Evaluate

We did NOT hands-on test Affirm with real loans or a live checkout. This review is based on the app's public store listing, its FAQ and changelog, its 4.8-star rating across 548k+ reviews, recurring themes in real user feedback, and Affirm's well-documented public reputation as a BNPL lender. Where the store copy makes forward-looking or marketing claims, we flag them as Affirm's claims rather than verified fact.

Pros & Cons

Zero late or hidden fees

Fixed, predictable payments

High-yield savings integrated

Real-time credit underwriting

Affirm Card for all stores

Rent payment flexibility

- ✕

Interest rates can be high

- ✕

Soft credit check required

- ✕

Late payments affect internal score

- ✕

Not all stores support Affirm

- ✕

Limited to larger purchases usually

- ✕

Requires US phone number

Download

FAQs

Does it hurt my credit?

Pre-qualification is a soft pull; taking a loan may affect your score.

Are there late fees?

No, Affirm never charges late or hidden fees.

How do I use the card?

Request a virtual card in the app and add it to your mobile wallet.

What is the interest rate?

Rates vary from 0% to 36% based on credit and retailer.

Can I pay early?

Yes, you can pay early at any time and save on interest.

Is there a spending limit?

Yes, your limit is determined by Affirm's real-time analysis.

Hot Reviews

I was able to get a new fridge without paying $1000 all at once. Life saver.

I love that they tell me the total dollar amount I'll pay. No math needed.

The Affirm card lets me split payments at the grocery store. So easy.

I was two days late once due to a bank error and they didn't charge me a cent.

The high-yield savings account is actually better than my local bank's.